Alcon: Will the allure of medtech spin-off work again? - Part 2

Continued from Part 1. This is a long read.

In part 1 of my post on Alcon, I provided some historical perspective on Alcon (ALC) and other medical device spin-offs. I will straight away jump onto why I believe that ALC can grow its earnings at 14% CAGR over the next 5 years and key growth levers for surgical and vision care business. I will talk about valuation in part 3 of my post on Alcon.

Growth levers for surgical business (56% of sales and 61% of EBIT)

Let me start with the surgical business which I expect is poised to grow ahead of cataract procedure growth rate of 5%. This growth will be led by new product introductions in the surgical implantables business of Alcon (28% of surgical sales; 16% of total sales). Surgical implantables business primarily consists of IOLs, which are artificial replacement lenses, placed in the eye following the removal of clouded cataract lenses. The IOL market has been witnessing an acceleration in uptake of premium/advanced IOLs. These Advanced Technology IOLs (AT-IOLS) account for 8% of IOL market units, but >30% of market revenues. An AT-IOL can cost 4x-8x more than a monofocal lens.

In the IOL market, share tends to shift rapidly with new product introductions because: (1) low switching costs, (2) IOLs can be used with all types of capital equipment, and (3) physician enthusiasm for new products is a significant driver of adoption (determined by clinical data and customer experience). These dynamics are best evident by looking at ~600 bps market share loss for Alcon in IOL market between 2015 and 2017 as ALC under-invested in the business while competitors launched new innovations in the market. Alcon’s implantable business grew 2% on average between 2010 and 2018, while the market growth was 6%-7% in the same period.

PanOptix, Alcon’s trifocal AT-IOL, is the most advanced IOL in the market with clinical data supporting that PanOptix is the best lens for intermediate vision with improved performance relative to other trifocal/bifocal/EDOF lenses and provides 85%-90% spectacle free rate after cataract procedure. Intermediate vision is important to users of tablets and other handheld devices (so becoming a key criterion in lens selection). A bifocal lens (two foci) improves vision quality over near and far distances but has issues with intermediate vision experience. A trifocal lens, like PanOptix, provides desirable results in near, far, and intermediate foci.

A study (https://pubmed.ncbi.nlm.nih.gov/27697256/) comparing PanOptix vs other trifocal lenses (PhysIOL – FineVision and AT LISA) concluded: “image quality performance of PanOptix was comparable to AT LISA and FineVision IOLs at distance and near foci, but the image contrast at intermediate 60 cm focus was significantly better for PanOptix compared with both AT LISA and FineVision.” Similarly, PanOptix delivered better results relative to EDOF lenses (Tecnis Symfony) with data indicating trifocals have better vision at near distances, compared to the EDOF lenses like Tecnis Symfony (which are optimized for intermediate vision) https://www.reviewofophthalmology.com/article/trifocals-and-edofs-where-do-they-stand .

Strong clinical data is supported by proven financial and customer satisfaction track record in Europe, Canada, Japan and now in US. Alcon launched PanOptix trifocal lens in Europe in 2015, with a full commercial launch in 2017. The company witnessed significant share capture with PanOptix growth of 2x the market in the Nordic countries (2Q17-2Q18) and 5x in Canada. PanOptix was 2nd trifocal and 4th multifocal lens in Europe with little to no coverage under any reimbursement arrangement in Europe. In the USA, PanOptix is the first trifocal lens with medicare allowing co-pay for a procedure with an AT-IOL (AT-IOL procedure costs ~2500-3000 out of pocket expenses per eye). The early evidence from USA shows significant strength for PanOptix, Alcon’s share has reached ~65% (within 10 months of launch) and 50-55% of global PC-IOL market, from ~25% just 2 years ago. Alcon's PanOptix launch in China (its 3rd largest market today) is on track, while its Japanese share is tracking above global average following recent launch (with likely room to continue ramping toward ~75%, similar to the US market share). Management is confident in reaching and maintaining a market leadership position in Japan given its dominant presence across most ophthalmology categories, and expects to be a #2 or #3 player in China.

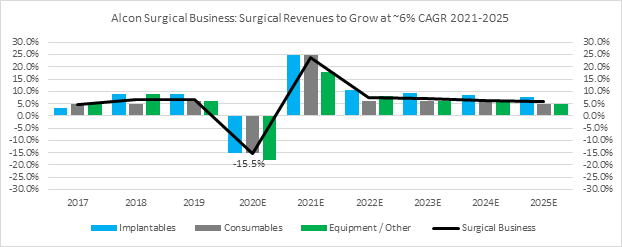

Further optionality, IOL portfolio beyond PanOptix: Alcon is also developing new IOL platforms that the company intends to launch in next 4 years. It is difficult to measure the revenue contribution of these new IOL platforms but the innovation pipeline remains strong, which will allow Alcon to grow its implantables business at 8% CAGR between 2021 and 2025, and gain market share in the process (market growth for implantables is expected to be at 6%).

A large equipment installed base creates an ecosystem that drives and supports growth for the entire surgical business while providing defensiveness to the business: Despite accounting for only ~9% of group sales, Alcon’s surgical device installed base provides considerable top-line leverage and a vital recurring revenue stream. For example, after the successful launch of the Centurion system, sales of IOL units to Centurion accounts grew 10% in 3Q14, whilst non-Centurion accounts experienced IOL unit growth of only 2%. This pull-through helps explain the consistent strength of the consumables business (30% group sales). Alcon has built an impressive share of the consumables market (discussed later), as it leverages its installed base to cross-sell disposables. ALC is notably strong in cataract equipment, especially phacoemulsification. Phaco machines are 95% of installed base in developed markets and provides Alcon an anchor in the account where the doctors are trained specifically on Alcon phacoemulsification machines. Once they’re trained on a certain technique and a certain device, doctors loath to change.

Equipment usually has 7-10 year life cycle; Centurion system, which is used in phacoemulisification during cataract surgeries, is in the late stages of its life cycle (introduced in 2013/2014) with new equipment introductions expected between 2021-23. Growth in the equipment segment will be driven by replacement/upgrade cycles as well as increased penetration in emerging markets. The growth is usually lumpier and highly correlated with new product introductions, as a result year on year trends can be volatile. I expect equipment business to grow at 4% CAGR as Alcon rolls out next generation of Centurion and Constellation systems, along with increased penetration in EMs where Phacoemulsification represent < 40% of the total cataract procedures (vs developed markets where Phacoemulsification is used in 95%+ of cataract procedures).

Alcon also sells procedure specific custom surgery packs, Alcon’s scale allows it to offer savings of c$50-60 per pack for new accounts versus a multi-supplier arrangement. Consumables is a relatively stable driver of growth, dependent on customer relationships and the installed base of primarily Phaco equipment. Alcon seems to have largely fixed its customer relationship issues that slowed the growth of consumables business in 2015-2016. Long term growth of consumables business varies with the growth rate of cataract and other ophthalmological procedures. Given the strong cadence of IOL and equipment roll-outs over the next 5 years, I expect consumables business to grow at 5.5% CAGR between 2021 and 2025, slightly ahead of 5% growth expected for ophthalmological procedures.

Covid-19 Impact on Surgical Business: Covid-19 has put a pause to the strong growth that Alcon’s surgical business has shown in 2019. Cataract procedures fell by 50% in April, though there has been sequential improvement in the data with sell-side channel checks suggesting procedures recovering to 70%-80% of pre-Covid levels. In US, the recovery should be faster as virtually 100% of all cataract procedures are performed in the outpatient setting with 75%+ of the procedures performed at ASCs. Infection fears will lead to postponement of surgeries by patients (given elderly population are most vulnerable to Covid-19) but most of the private ASCs have financial incentives to maintain high utilization rates of their eyecare facilities.

Also, I do not expect significant trade down to monofocals; cataract surgery is once in a lifetime surgery, and elderly population has more savings and less debt with low impact from rising unemployment (no evidence of down trading in last recession).

On the equipment side, Covid-19 will put pressure on equipment sales in 2020 as the hospital capex will remain benign given low ER and elective volumes. I do not think there will be medium term demand destruction as increased elective backlogs next year will mean increased focus on OR efficiency, and prioritization of elective surgery related capex over some other forms of capex. Lastly, I expect consumables volume will recover as the surgery volumes rebound in 2021. Overall, I expect that due to Covid-19, surgical sales will fall by ~15% in 2020 (H1 impact has been -23%) with a snap-back in 2021 as the backlog builds-up and little risk of down trading.

I expect surgical revenues to grow at 6% CAGR between 2021-2025 (2021 growth number normalized by taking average of 2020 & 2021 growth), driven by strong innovation pipeline.

Vision care business - Precision 1 fills a hole in Alcon’s contact lens portfolio. Flexible manufacturing system will accelerate roll-out of new contact lenses.

Alcon is the joint number two player in the $8bn global contact lenses market with ~24% market share. The global contact lens market grew ~5% in last 5 years with multiple structural tailwinds: a) shift to SiHy (silicon hydrogel) lenses, which have become 69% of the total US contact lens market and sell at 20% premium to traditional hydrogel lenses, b) continuous shift to daily modality (53% of market) from monthly/weekly reusable lenses, c) move from spherical to toric and multifocal contact lenses (selling at 15%-30% premium), and d) international expansion as the penetration of contact lenses in emerging markets is still at 3% vs 16% in USA.

Contact lens market is “sticky”, with patients usually transitioning from one lens to another more through dissatisfaction with a current lens than because of marketing campaigns and product rebates. Despite this, Alcon has been a share donor due to lack of product launches in key growth segments of the market and capacity shortfalls. ALC failed to grow at the pace of its two key competitors, exhibiting a 2015-18 CAGR of 3.3% vs. c. 8% for Cooper Vision.

Alcon’s dailies portfolio is dominated by DAILIES TOTAL1, premium daily SiHy contact lens product (~$800 per year per user), with DAILIES AquaComfort PLUS lenses towards the lower end of the value segment with ~ $200 per year cost for the user. Precision1 will be Alcon’s SiHy dailies offering in mid-price segment. Mid-range segment accounts for as much as 40% of the overall dailies market, and has been the fastest growing segment of the dailies market. Management expects Precision1 will become biggest growth driver in the daily segment, with a global roll-out expected in 2021 and will overtake DT1 by 2023E while only cannibalizing 15-20% of DT1.

Apart from Precision 1, new products like DT1 toric (used to correct astigmatism) and multifocals are expected to be launched in the US market in 2021/2022. These line extensions are important, for instance, Cooper Companies (ticker COO) has stated that it was only after the launch of a toric equivalent of its premium daily lens in March 2018 that sales of the line started to accelerate. Alcon’s delay in launching toric lenses has been a result of continued capacity constraints which have been largely resolved now. Alcon is transforming its vision care franchise to a flexible manufacturing facility, a universal platform to manufacture multiple types of lenses and chemistries on the same manufacturing line. This manufacturing facility will not only ensure faster roll-out of Precision 1 but also allow simultaneous launch of toric and multifocal lenses. The new contact lens platform is expected to have ~40% improved output per line, ~40% lower cost per lens, ~35% lower capex per line, and create a sustainable platform for Alcon to innovate at an accelerated pace.

In the reusable segment, Alcon is well established with its Air Optix range. The Air Optix family includes replaceable lenses in monofocal, astigmatism correcting, and multifocal options and also includes the Air Optix Colors cosmetic lenses. Alcon’s reusable lens business has been flat due to switch to daily disposable lenses.

Impact of Covid-19 on Vision Care: Although new contact fit trends have improved from April lows, volumes are still down ~25%-35% versus baseline. Lack of many seasonal for new fits (i.e. weddings, proms, graduations), fears of respiratory droplet and tear film transmission are keeping new adoption volumes depressed. Some of the demand would have shifted to online channels, but new fits on which Precision 1 is dependent to gain new customers have slowed. Additionally, some sell-side checks are suggesting evidence of steep rebates. For instance, J&J led with a $300 rebate for a 1-year supply of Acuvue Oasys dailies vs. $225 for new wearers and $100 for existing wearers. COO followed suit with rebates of $200 and $150 for a 1-year supply of MyDay/clariti versus the current $130 offer in place through June 30. I expect contact lens business to come under pressure this year due to recessionary pressures as well as increased discounting to offset those pressures. Therefore, ALC’s contact lens business will under-perform its peers in 2020. I model sales down 15% in 2020, with a snapback in 2021.

In Ocular Health, Pataday and pantry loading has derisked the year (23% growth in Q1), I expect 3% Ocular growth in 2020.

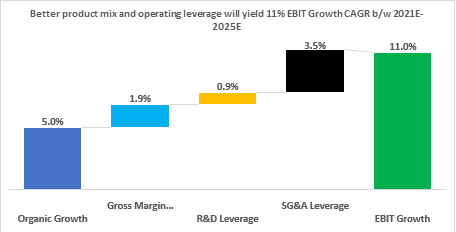

Depressed operating margins should recover by 500 bps due to favorable product mix and operational leverage.

Alcon’s operating margin fell from 22.3% in 2015 to 17.1% in 2016 and 16.0% in 2017 as the company increased investments in sales, marketing, and R&D to turn around the business. For example, SG&A as a percent of sales jumped from 34% in 2015 to 38% in 2016-17. During that period, Alcon’s gross margin also suffered – falling 100bps from 2015 to 2017 – from lower sales due to market share losses and manufacturing inefficiencies. Post the period of accelerated reinvestment margins recovered partially in 2018 and 2019. The company has also been investing $400-$450MM per year to implement a global SAP system and build a new flexible contact lens manufacturing line (these investments are in final stages, and should normalize beyond 2020). Covid-19 has pushed management’s margin targets by 12-18 months, but I expect the margins to reach 22% by 2025. This margin expansion will be result of 200 bps gross margin expansion and 500 bps of core EBIT margin expansion.

Improvement in gross margins driven by product mix & manufacturing efficiencies.

Daily contact lens wearers provide 3-4x the revenue and 2x the profit relative to reusable contact lens wearers. Shifting from reusable to daily modality is gross margin dilutive in the short run but becomes accretive as production efficiency ramps-up. Cooper Companies has stated that a typical daily lens commands a ~55% gross margin versus over 70% for reusable sets. COO’s management disclosed in 2016 that after substantial investments in daily contact lens manufacturing in 2014-15, gross margin returned to pre-investment level four years later.

Unlike Cooper, Alcon has already done most of the investment in manufacturing efficiencies. The new flexible production lines will reduce the dilutive impact of dailies lenses on gross margins, these lines could generate an increase in output of ~40% and a reduction in cost per lens of ~40%, it is likely these projects will be completed by 2020 and could become margin accretive in 1-2 years.

On surgical side, AT-IOLs have approximately the same COGS as monofocals but 3-4x (for toric) and 6-8x (for multifocal) the revenue. The margin differential between AT-IOL and monofocals is significant (~90% v/s 75% for monofocals). Surgical division gross profit margins will improve as new product launches become a bigger part of the business relative to monofocals and this partially offsets inventory build-out in the IOL business and pricing pressure on monofocal lenses.

Operating margin expansion due to normalization of expenses and better cost absorption with a growing top-line.

Analyzing operating margins of Cooper Companies and Carl Zeiss – provide insights on Alcon’s steady state EBIT margins. COO (vision segment constitutes c. 78% of top line in 2019) represents the best comparison for Alcon's Vision Care business, and Carl Zeiss (73% revenues from Ophthalmic Devices) is closer to Alcon’s Surgical business. Comparing the Core Operating margins of these three companies highlights two key takeaways:

1. Alcon is in line on R&D spend, which appears to be driven by the Surgical business: While COO's R&D margin (as a % of sales) ranged from 3-4% from 2015-19, Carl Zeiss' R&D margin ranged from 11-12%. This suggests that Alcon's Surgical business is the primary driver of R&D spend. Competitor weighted average R&D margins (ranging 6-7%) are broadly in line with those reported by Alcon (7%). ~7% R&D as a % of sales will be sufficient to support MSD organic growth, this is what management has been guiding as well.

2. Room for improvement on SG&A spend, which appears to be driven by the vision care: The Cooper Companies has reported higher SG&A margins (as a % of sales) vs. Carl Zeiss, which suggests that Alcon’s Vision Care business is the bigger driver of SG&A spend. Alcon's top line is 1.8x that of Cooper Companies’ vision division and 3.5x that of Carl Zeiss’ Ophthalmic Devices segment in 2019, which should allow Alcon greater leverage over fixed costs. Notably, Alcon’s SG&A spend has consistently been higher than competitors (Cooper @ 36% and Carl Zeiss @ 27%), going forward I expect SG&A spend increases at 3%-3.5% rate which will mean ~350 bps leverage from 2019 levels of 38%.

Overall, I expect ALC to hit 22% core operating margins in 2025, which will provide 11% EBIT growth CAGR between 2021 and 2025 (I am calculating 2021 EBIT growth using 2019 as the base rather than 2020).

Further peer benchmarking supports a mid-20s number:

J&J’s vision business – which is the most direct comparison for the whole of Alcon, given that the business spans both surgical ophthalmology and vision care markers – earns a 27%-28% margin before overhead/corporate costs; assuming 200-300 bps of corporate costs, JNJ’s vision margins are 24%-26%, well above Alcon’s 17.2% group core EBIT margin in 2019.

Cooper reported an adjusted EBIT margin of 27.7% in FY18; this compares with Alcon’s contact lenses margin of <19% (2018) excl. corporate costs; and

Prior to being acquired by JNJ, the Abbott Medical Optics business – which consisted of products for cataract surgery, laser refractive surgery, and consumer eye health – was earning a 22%-24% adj. EBIT margin; this compares with a 21% margin for Alcon’s surgical business in 2018.

In summary my investment thesis on ALC is based on following three thesis points:

1) PanOptix driven strong AT-IOL growth supported by leadership position in surgical device market will allow Alcon to grow its surgical business ahead of market.

2) Precision 1 fills a hole in Alcon’s contact lens portfolio; flexible manufacturing system will accelerate roll-out of new lenses.

3) 500 bps EBIT margin expansion by 2025 due to favorable product mix and operating leverage. I expect EBIT growth of 11% CAGR over next 5 years.

This post is already too long, therefore, I have decided to discuss valuation in part 3 of my post on Alcon.