Sum of the parts valuation of Philip Morris International

Sum of the parts valuation of Philip Morris International

Philip Morris International (PM) has been a special case in the tobacco world. The company has invested vast amounts in innovation over the past six years, to disrupt its own core cigarette business and created an entirely new heat-not-burn (HNB) category in the process. Cigarette business is still ~78% of the revenues but the company has a vision to move towards a smoke-free future through its portfolio of reduced risk products (primarily IQOS). PM has spent over $2billion commercialize IQOS over the last 4 years. This process of investment has been painful – margins were down 7% pts between 2012 and 2018 due to a step-up in IQOS investment. The fixed-cost infrastructure is now in place, and PM will be reaping the benefits as IQOS scales-up. Traditional cigarette business continues to be LSD revenue growth business. IQOS business (expected to be 25% of revenues in 2022) is the growth engine of the company with market and technological leadership in heat-not-burn category across the world. If you want to go through my thesis on PM please refer to my twitter thread (PM bull thesis).

A question that I often get from investment community is on appropriate multiple for the stock and how much are we paying for IQOS growth. All these are valid questions, especially when ESG and regulatory concerns can make one feel that no price is low enough for a tobacco stock.

To arrive at SOTP valuation for PM it is important to have some historical context on both Philip Morris International and tobacco industry. PM was carved out of Altria (MO) in 2008 as the high growth international business with little exposure to US regulatory environment (for more details read WSJ article on PM/MO split). The core cigarette portfolio of the two companies is very similar and therefore, two stocks were considered close and best comparable for each other.PM still does not have any exposure to US cigarette market so any regulatory actions by FDA does not directly impact PM’s profit pool. Of course, FDA actions can become basis for future regulatory actions by regulators outside the US.

The best way to arrive at a multiple for the combustible portfolio is to look at what has happened to the valuation multiples of tobacco stocks over the last 10 years. I view last 10 years as two distinct phases which differ from each other in terms of regulatory risks and competitive cadence from reduced risk products.

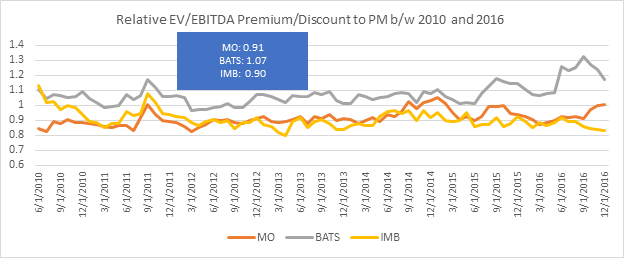

Phase 1: Benign regulatory environment and no major competition from reduced risk products (b/w 2010 & 2016): During Phase 1 regulatory environment on tobacco was benign or more appropriately focused on abstinence-only approach (i.e. regulators focused on generating awareness that tobacco is bad and restricted its sales/marketing in certain manner). Obama administration approved Tobacco Control Act in 2010 which gave FDA explicit power to regulate tobacco industry, but investors largely brushed aside this change in regulatory stance or at least such risk was not reflective in the valuation multiples of the stocks. In fact, between 2010 and 2016 Altria (MO) outperformed S&P 500 by a big margin (MO gave a return of 245% vs S&P 500’s 100% return).

During most of Phase1, IQOS and other reduced risk products like e-vapor (JUUL being the prime example) did not pose a major existential threat to the combustible cigarettes. For instance, PM sold 400 mm Heets (Heets is used with IQOS) in 2016 vs 813bn cigarettes that year. JUUL, launched in mid-2015, was also too small to make a meaningful impact. JUUL’s social media mentions were fairly non-existent for much of 2016 (remember social media was an important part of JUUL’s growth strategy).

As a result of these dynamics tobacco stocks traded largely in line with consumer staples sector and broadly speaking historical tobacco algorithm was working as expected with cig. volumes declining by 2%-3% offset by pricing of ~5%, providing LSD organic growth, MSD EBIT growth & HSD/LDD total shareholder return.

Between 2010-2016, MO traded at ~9%-10% discount to PM despite having similar product portfolio - I attribute this premium to a better management team and exposure to faster growing geographies. Overall, I categorize Phase 1 as the period of little competition from alternative products and a period of limited regulatory action. All this was getting reflected in the valuation of the sector as stocks traded at valuation close to consumer staples stock.

Phase 2:Negative regulatory news flow with accelerated volume declines – era of great tobacco de-rating: On July 27, 2017 FDA released its proposed rule-making agenda for tobacco industry which had industry disruptive ideas such as nicotine product standard in US along with an agenda to ban menthol cigarettes (click here for details). This took industry by surprise and the stocks fell 7%-10% on the day, it was also the beginning of the broader de-rating of entire sector and stocks still trade at these 30%-40% depressed multiples to this day.

If the existential threat to the industry was not bad enough there was a new problem that started to take shape: meteoric rise of JUUL. JUUL used questionable marketing practices and became a widely popular product, especially among teens (here is a TIME article on the topic). Increase in prevalence of teen nicotine usage did not bother big tobacco that much as teen smokers account ~2% of industry volumes. The problem was that JUUL was a better product and less harmful as it did not have tobacco in it. This not only attracted teens but also many adult smokers started switching to JUUL – cannibalizing cigarette volumes in the process.

JUUL ended up becoming ~5% of total nicotine market by fall of 2019. All this led to accelerated volume declines for cigarettes at 5.3% in 2018 and 6% in 2019. Pricing accelerated to 8%-9% to compensate for this accelerated decline in volumes. As a result, multiples for BAT, Altria, and IMB decoupled from staples multiples, leading to a 30%-40% de-rating of the sector. I believe these multiples appropriately reflected the scenario that the highly cash generative tobacco algorithm is broken and HSD pricing adopted by tobacco players to offset volume declines is not sustainable. Between 2017 and 2019, S&P 500 and XLP (consumer staples ETF) returned 46% and 21% respectively but MO and PM returned -26% and -7%.

JUUL ultimately ended up becoming victim of its own success with youth tobacco survey of 2019 highlighting alarming rates of usage of e-cigs among teens. Regulators decided to crackdown on JUUL and the company is currently part of many investigations (JUUL investigations). All this negative press for JUUL ended up becoming a blessing in disguise for big-tobacco companies. Cigarette volumes have recovered in 2020 as JUUL dialed back its marketing practices and restricted sale of flavored products (JUUL will stop selling mint e-cigs).

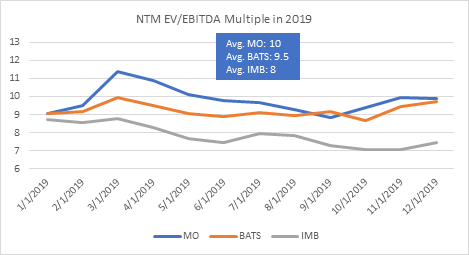

All this analysis/history was necessary to understand why using a 5 year/10 year avg. multiple for the sector can provide a sense of false margin of safety. The right window to look at is between 2017 and 2019 (or Phase 2). Even within Phase 2, the pain was maximum in 2019. Looking at 2019 trading multiples (the worst year b/w 2017-2019) for PM’s competitors can provide a benchmark to arrive at the appropriate multiple for PM’s traditional combustible business. As highlighted above, this was the peak pain period for US focused tobacco players with Juul and regulatory environment pressuring fundamentals and valuation to maximum extent. MO traded at a 10x multiple (after adjusting for investment income) in 2019, while BAT traded at 0.5x discount due to higher leverage (BAT generated 4% revenues from reduced risk products which I consider insignificant). Imperial had company specific execution issues with a dividend cut expectation baked into the multiple (dividend cut happened in May 2020).

Out of the 3 competitors, I think MO is the best benchmark for PM’s traditional combustible business as the two companies have similar combustible product portfolio. Historically (b/w 2010-2016 when IQOS & regulation did not pressure tobacco multiples), MO traded at 10% discount to PM. There were three main reasons for this discount: a) less risk of adverse regulatory action (PM does not have a US profit pool), b) exposure to high growth markets outside the US, and c) PM has a better management team with a stellar track record of capital allocation (compare this to Altria, which invested $13 bn in JUUL and wrote it down by 40% within 12 months of investments). Therefore, Altria’s 2019 average forward EV/EBITDA multiple provides a good lower bound for PM’s traditional tobacco business. If I apply the historical 1 turn or 10% premium to MO’s 2019 forward EV/EBITDA multiple, then I arrive at 11x EV/EBITDA multiple for PM’s tobacco business.

Given improving cigarette volumes and JUUL becoming increasingly irrelevant, a case can be made for the re-rating of the entire tobacco sector. I will refrain from that discussion here, 11x forward EBITDA multiple for PM’s cig. business is my conservative estimate for the cigarette business.

IQOS Valuation: IQOS constituted 20% of PM’s revenues and generated $5.5 bn in revenues in 2019 (IQOS will be 25% of sales by 2021). It had 17% market share of tobacco category in Japan, and near monopoly position in all other markets (6% market share in Italy, and ~5% in Russia). IQOS growth in FY2020 will be HSD; most of IQOS stores remain shut because of Covid but I do expect the growth to return to 20%+ levels in FY2021 and FY20222. Overall, IQOS remains a mid-teens grower (14% CAGR) over the next 5 years as there is significant room to double the current penetration levels outside Japan. Moreover, the peak investment period for IQOS in largely over, this can be seen from lower customer acquisition cost.

Given IQOS’ growth potential, the closest proxy to IQOS is Swedish Match (SWMA). SWMA is exposed to risks and opportunities similar to IQOS, these risks and opportunities are:

1) SWMA is a tobacco player that derives 70% of its revenues from reduced risk products (snus, moist snuff, and oral tobacco). Rest 30% is from mass market cigars in US, of which 45% is from flavored cigars that may face regulatory action in near future. Therefore, ~87% of the SWMA’s business is not exposed to any adverse regulatory action. IQOS given its reduced risk credentials (95% reduced risk) is also largely insulated from any adverse regulatory action. IQOS became MRTP certified a month ago which further reinforces its reduced harm claims (IQOS gets MRTP).

2) Like IQOS, SWMA has a fast-growing reduced risk product (Zyn) which is disrupting an existing profit pool. Both Zyn and IQOS get favorable tax treatment from regulators due to their reduced risk credentials. There is a risk that with time these tax advantages for IQOS and Zyn will be phased out which will reduce the potential attractiveness of Zyn/IQOS.

3) Similar business model – high cash generation, clean balance sheet, ~40%+ operating margins etc.

SWMA currently trades at ~15.5x NTM EV/EBITDA which provides a lower bound for IQOS valuation. IQOS should be valued at a premium to SWMA given higher growth rate and no risk of adverse regulatory action i.e. 13% of revenues not at risk of being banned by the regulators. If I back out the multiple for the 70% of reduced risk portfolio of SWMA, then the appropriate multiple for IQOS will be 19x. (I assign 7x multiple to cigar portfolio – this is where IMB trades right now – and then calculate implied multiple for non-cigar portfolio that will get me to 15.5x EV/EBITDA for SWMA as a company). SWMA’s non-cigar business or reduced risk business is expected to grow at 7%-9% CAGR over the next 5 years, which is still significantly lower than 14% growth for IQOS over the same period.

Putting it Together: The table below shows the price at which I arrive for PM’s stock if I value combustible and IQOS b/w the lower bound and the justified multiple based on my analysis (11x for combustible and 19x for IQOS). My margin of safety is that my lower bound multiple for combustibles business represent the peak pain period for tobacco stocks. 19x forward EV/EBITDA multiple for IQOS represent the implied multiple for SWMA’s non-cigar business (which grows 40% slower than IQOS).

December 2021 valuation of $90 for PM represents 17% upside from the current price of $77. This price will imply a 13x forward EV/EBITDA multiple for the whole company on my 2021 EBITDA estimates. If you include 6% dividend yield, stock can generate 23% total shareholder return over the next 15 months.

Please feel free to let me know if you think differently about the valuation of PM’s stock or PM as a business.